What a difference a week makes. The Reserve Bank's OCR announcement release last week came with a major shift in tone. The RBNZ did

not adjust the OCR setting as expected, to the disappointment of many businesses that are struggling (and many economists hoping for

the bank to look forwards and not backwards), however the bank acknowledged that the economy has worsened quicker than they had

predicted, much to the the surprise of nobody who actually works for a living. Predictions for OCR cuts quickly shifted from

"sometime late next year" as of their previous release, to this

side of Christmas.

What made the RBNZ change it's tone?

Two things:

A lot of already weak economic data got worse, pretty much all at once

Our month-on-month inflation data pulled

right back.

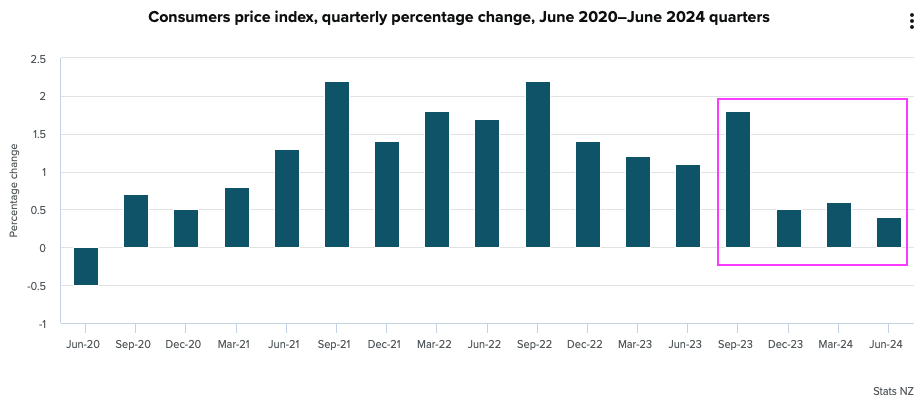

Our CPI is comprised of the four previous quarters and aore than half of the total 3.3% of the quoted 12 months of CPI was baked in

more than 9 months ago, as you can see from the below quarterly CPI charrt.

Job

ads

and building

consents are down, as

is freight,

inflation-adjusted consumer spending is down, and there are a lot of stories in the news about local businesses, especially hospo and

tourism, doing it tough. It's hard yakka out there and there don't seem to be many shining lights in the economy. The RBNZ acknowledged all

of this and basically hinted that rates might need to be eased much sooner.

Straight after the OCR announcement, financial markets shifted to pricing in interest rate cuts this year, banks lowered term

deposit rates, and over the last week most banks have started to reduce their interest rates on offer.

What does that mean for property?

Beyond the obvious relief that holding costs are going to go down, at the coalface we saw an immediate change. Our Rotorua sales team in iSellProperty

noticed an immediate bump in interest; on a wet Sunday most of our open homes saw more people through than that last 4 weeks

combined.

Very small sample size? Yes, it couldn't be smaller. Will prices rocket away soon? Absolutely not, the economy usually turns at the pace of

an ocean liner, not on a dime :-)

What it does signal is folks are feeling that they can buy with more confidence now that the RBNZ appears to have done its

thing. We are still in the winter and the painful after-effects of this tightening cycle will take quite a bit more time to play out,

so monthly data will bump along the bottom for a while. However, at the macro level it feels like there is a floor in place

now and more people will plan for the future instead of hunching down and waiting for it all to be over.

What do I think will happen?

There is a saying that the RBNZ shows up too late for every party, does too much, and stays too long. That was certainly the case with

how long low interest rates were left in place, and I feel they have overcooked their response too and left the OCR high for longer

than needed to take heat out of the economy.

The economic pullback will probably end up deeper than the bank would have anticipated, and the only thing that

might prevent a sharper-than-predicted decreases in OCR is the fear of inflation making an unwelcome return.

In short, I think the pull back has been faster than the bank anticipated and will require an equally fast economic response. Don't be

surprised of rates drop more and sooner than the latest round of economist predictions.

Are we in a "good" buyers market?

I think we are. A "buyers market" is when there are more buyers than sellers and buyers have time and choice. That has been the

case for a while now, however we have shifted since the change of government to what I call a "good buyers market" - where the

above holds true, but policy changes that are outside our control won't make things worse, so a buyer can invest with more

certainty.

I believe we have perhaps a 12 month window, where buying will be quite good (and news cycles will be grim).

Looking through the bad news still to come, once market confidence - particularly jobs confidence and consumer spending - returns,

I believe the baked in wage increases from the last few years will combine with lower interest rates and values will lift again.

Recently introduced DTI limits may hold the market in check in the future, but it will be in check at the top of a range, and not where

things are at now.

In 2022 I published a two-part series on inflation (part1,

part2). We are just coming out of

a sharp increase in rents, which I mentioned in part 2, and I believe we will soon see the big benefit of inflation, erosion of

debt, materialize as interest rates come down.

My advice to investors

From someone who invested through the GFC and got a bit wrong, as well as a bit right, and has had many years to reflect and grow, here are

some tips:

Be ready to buy. There will be good deals and more active buyers, so you will want to be in a position to pounce. So go talk with that

advisor, meet with an accountant, and set your mindset that you are in the market.

Join the local property investors association and start to chat with people each month about what they are doing. You will pick up what to

be optimistic about and wary of from experienced people.

Don't rush out and get stuck on an average-to-bad deal. Your likely biggest risk in this market is opportunity cost of having to watch from

the sidelines.

Have a goal you are working towards, each purchase has to contribute to that goal. There will be deals that work for others but not

you and that's OK.

Know that the news will be bad about the economy for a while yet. Mentally allow for it in advance.

Understand what it will take from the bank's perspective to build a portfolio.

Work with a coach, mentor, buyers agent or some other expert to make sure you don't settle for mediocre

and watch the market leave you behind.

Hamilton has never been about hype, it’s a market built on something far more valuable to long-term investors: steady demand,

consistent performance, and reliable tenants.Read More…

While Tribunal applications remain uncommon for our clients, these cases reinforce the importance of good documentation, strategic

decision-making, and experienced representation.

Read More…

In property management, “busy” is easy. The phone rings. Emails flood in. Maintenance requests stack up. Tenants need answers. Owners want

updates. At iRentProperty, we believe productivity isn’t about doing more. It’s about doing the right things, at the right time,

to protect and grow our clients’ investments.

Read More…