During a crisis the goal is hold onto your assets and acquire more as you can, while sticking to rues and maintaining some flexibility.

As a property investor it is about access to cash in the immediate term to handle a painful vacancy or job loss and cashflow is critical

for the duration.

The Now - Cash or Access to Cash (your insurance policy)

The immediate term is right now; the government put in rules to prevent ending a tenancy for obvious reasons,

however some folks are not paying rent or are paying reduced rent. This is temporary and things will stabilize at some new level when

people can move around again and the new work normal becomes apparent.

Other owners have found they got caught out by the lockdown and have had to hold a property vacant for a spell.

Cash helps you navigate this kind of turbulence (same as any business).

The banks have tools to help owners through this:

Interest only loans

Extending the repayment term

Revolving credits

Repayment deferrals

Etc...

While a deferral is expensive, it is cheaper than losing the asset and solves the "access to cash" problem for 6 months.

A friend took a repayment deferral for 3 months and it adds about $3pw for the rest of his loan... people are thinking about these the way

they buy homes, not total cost but more "can I afford the repayments".

Anyway, I call this insurance because while you never want to have to use it, it is good to have when you need it.

I extended my revolving credit the minute this thing broke. Both as a defensive mechanism and I always want to be in position to buy.

Going Forward - Cash flow

Property investment is all about smart leverage (anyone who says it isn't is trying to sell you something) and rule # 1 is that you cover

your costs.

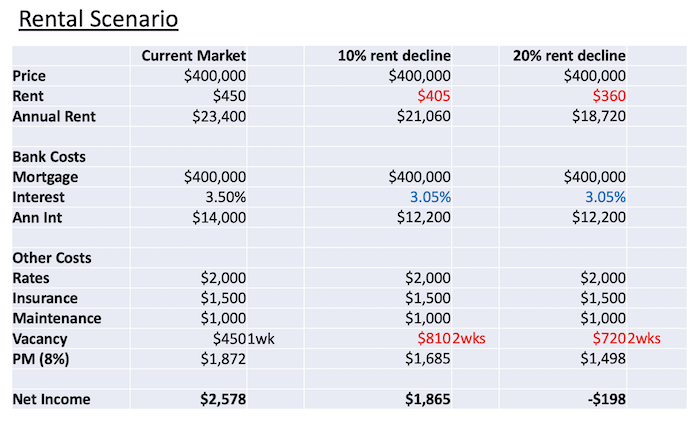

Rents are likely to soften in some areas, particularly expensive resort towns where a lot of housing had gone to Airbnb or work has dried

up, however interest rates, which by far are your biggest cost, have also crashed to 3% (so a 20% drop).

I did some rough maths and saw that even if you borrow 100% of a property costs, once you can get your loans to the lower rates, a drop in

rents won't really move the needle, certainly not enough to tip investors over. Note that below I have also added a week of vacancy to the

decline scenarios.

What will lead to long term strife for investors is if their cashflow was poor from day 1, they borrowed (perhaps against property)

to fund a business that is in trouble, or they lose their own source of employment, need to pull back to save their own homes and the bank

decides what happens to the proceeds form a sale (and not you). So multiple bad things happening at once...

What makes this crisis so hard to watch from a purely economic perspective is people who didn't over-speculate by any traditional metric are

going to get hurt.

By comparison, having to drop your rent by $20-50 pw for a couple of years isn't going to make any difference whatsoever. In fact the last

time houses were flat/cheap during the GFC it was relatively common and those who simply got on with it did very well

Much like KiwiSaver balances, property values won't affect you if you don't have to sell and can pay your loans.

If you detect a whiff of trouble look at ways to add access to cash well before you need it and I always recommend going through a good

broker to manage communicating with the bank.

Looking forward.... there may be price drops in some areas, who knows at 3% interest rates and QE about to hit. Entering the GFC

interest rates were 10% and there had been a lot of risking lending leading up to it. This time rates are low and serviceability testing

already in place means people have to have good cashflow and equity in place to buy more than 1 or 2 rentals most of the time. It is a very

different world.

My plan is to keep buying when and as I can. Some people will wait and wait and maybe buy something and by then active investors will have a

good portfolio and will be accelerating. You become wealthy from having portfolio, not by timing market swings for a single purchase.

I am not a financial advisor. Please do your own due diligence and use your team (broker, accountant, planner) to help you plan the path

that works for you.

Hamilton has never been about hype, it’s a market built on something far more valuable to long-term investors: steady demand,

consistent performance, and reliable tenants.Read More…

While Tribunal applications remain uncommon for our clients, these cases reinforce the importance of good documentation, strategic

decision-making, and experienced representation.

Read More…

In property management, “busy” is easy. The phone rings. Emails flood in. Maintenance requests stack up. Tenants need answers. Owners want

updates. At iRentProperty, we believe productivity isn’t about doing more. It’s about doing the right things, at the right time,

to protect and grow our clients’ investments.

Read More…